Jimmy Pickert, CFA, CRPS® Portfolio Manager

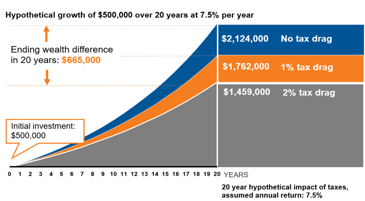

Tax-loss harvesting is one of the most well-known tax tactics for investors. It is the process of selling an investment that carries an unrealized loss. The loss realized by the investor can be used to offset realized gains elsewhere. Additionally, up to $3,000 of realized losses can be deducted from ordinary income per year, and any unused losses in a year can be carried forward indefinitely under current tax law.

Where most investors get hung up on this topic is their reluctance to sell and make their loss permanent. This is sound thinking—after all, Investing 101 tells us that we should buy low and sell high, not the other way around, and additionally that we shouldn’t sell out of our investments in the middle of a bear market. You might ask, “Well, what if I sell this stock and just buy it back right away?” Fair question, but the IRS has anticipated that loophole by creating the Wash Sale rule. If you sell an investment at a loss and then buy it back within 30 days, you don’t get to use that loss to reduce your taxes. This creates a dilemma because no investor wants to see the investment they just sold rally higher during that 30-day window.

The solution to this dilemma is to purchase a similar, though not identical, investment immediately after the sale of the original. A simple example can be used to demonstrate this process. You currently own shares of Coca-Cola stock, and your position in that stock has a loss of $10,000. You can sell your Coca-Cola stock and immediately buy Pepsi stock with the proceeds. The end result is that you have harvested the $10,000 loss, thus accruing a tax benefit, and have meanwhile stayed invested in the market in case there is a rebound in the soft drink industry over the next 30 days. After 30 days, you can either swap back into Coca Cola or you can stick with your new Pepsi stock. By the way, tax-loss harvesting is not limited to individual stocks. Is your diversified mutual fund trading at an unrealized loss? You can sell it to harvest that loss and replace your exposure with a similar mutual fund or exchange-traded fund.

Many investors review their portfolio in December each year to identify opportunities for loss harvesting, but another great time to do this is in the wake of a market correction or bear market like we saw in the early Spring of 2020 at the beginning of the pandemic crisis. Are you worried your portfolio may not be taking advantage of this strategy? Contact ACG to see how we can help.