Bobby Moyer is the Chief Investment Officer at ACG. Jimmy Pickert is our Portfolio Manager.

See our recap of February's key statistics and market commentary below.

Noteworthy Numbers

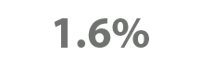

The yield on the 10-Year Treasury Bond reached as high as 1.6% in the last week of February as investors began to focus on the impacts of a recovering economy and the potential fiscal stimulus on interest rates and inflation.

The yield on the 10-Year Treasury Bond reached as high as 1.6% in the last week of February as investors began to focus on the impacts of a recovering economy and the potential fiscal stimulus on interest rates and inflation.

Our Take

The S&P 500 finished positive in February, gaining 2.76%, although the month looked similar to January in that a robust first few weeks gave way to heightened volatility and losses towards the end. Small and mid-sized companies in the U.S. outperformed the large-cap based S&P 500 during February. Value stocks outperformed growth stocks by a wide margin in a continued reversal from last year’s trend. Perhaps most remarkable, if not surprising, has been the rapid rise in interest rates so far this year and the difficulties that that has presented to bonds. The Bloomberg Barclays Aggregate Bond index lost value in both January and February this year, with the index now negative for the year by -2.15%.

It is important to be specific when discussing the increase in interest rates. After all, yields on the shorter end of the yield curve (the 3 Month, 1 Year and 2 Year Treasury yields) have not risen but actually fallen slightly since the beginning of the year. The short end of the yield curve is predominantly influenced by the Federal Reserve, and because the Fed continues to keep its own Fed Funds Rate at zero, these shorter-dated yields have not seen much movement from their current historic lows. By contrast, the longer end of the yield curve (the 5 Year, 10 Year and 30 Year Treasury yields) are influenced much more by the economic outlook and future inflation expectations. Yields on the long end of the curve have increased substantially so far in 2021; the yield on the 10 Year Treasury closed 2020 at 0.92% and rose all the way to 1.45% by the end of February. This is a substantial move over two months.

Recent interest rate movements shouldn’t be viewed as wholly good or wholly bad for the markets and the economy. On the one hand, a steepening yield curve—what we’ve seen over two months—is a clear sign that economic expectations are improving. Long time readers of this newsletter may recall that at the end of 2019, the primary concern was that the yield curve would invert—that short yields would be higher than long yields—which has been a historically reliable predictor of imminent recession. As our economy continues to recover from COVID-19, a recovery that vaccine efforts will hopefully accelerate, it only makes sense that we would see the yield curve steepen. Additionally, a steeper yield curve is great for the Financials sector. The primary M.O. of banks is to borrow money at lower short-term rates and lend that money out at higher long-term rates. Thus, it is not surprising that the Financials sector is the second-best performer in the S&P 500 this year, positive by 9.63% for the year (Energy is the best performing sector, partly based off gains from last year’s lows but mostly driven higher by the energy crisis in Texas).

On the other hand, higher long-term rates are stoking fears around inflation. Admittedly, inflation has been expected-but-absent throughout the past decade plus, as economists kept waiting for the Fed’s long lasting accommodative period to spur prices higher. However, many expect that pent-up demand and supply chain disruptions as a post-COVID economy comes back online may be enough to usher in a new period of higher inflation. The latest release of the Core Consumer Price Index (CPI) showed a year-over-year increase in prices of 1.4%. While this is still below the Fed’s target of 2% inflation, the rapidity of the yield curve steepening combined with the effects of post-COVID normalization have many observers worried that we could blow past that 2% target soon.

Another impact of higher interest rates is on valuations. Whether we’re speaking of stocks or bonds, the intrinsic value of an investment is determined by discounting its future cash flows at the prevailing interest rate at the time. This is easy to see with bonds, where all future cash flows are predetermined in the form of interest payments and the maturity; this is the fundamental reason why bond prices decline when interest rates go up, and vice versa. But the same holds true for stocks. As interest rates increase, the intrinsic value attributable to future earnings and dividends decreases. With interest rates increasing over the past two months, stock analysts have had to readjust their valuation models. Much of the stock market’s volatility at the end of February appears to be driven by the impacts of these higher interest rates and the potential advent of higher inflation.

It will be interesting to see in the coming months how sentiments around inflation develop. As a result of much lower inflation during the Spring of 2020 as COVID-19 began disrupting the global economy, there is a high probability that monthly data will show year-over-year inflation growing at higher than 2% as we enter the spring and summer this year. Will market participants interpret this as a temporary blip caused by last year’s low baseline, or will they view it as the beginning of a new period of high inflation? The answer to that question may define the stock market’s trajectory over the next few months.

Get Monthly Insights Delivered to Your Inbox

Subscribe to our Investor Insights Newsletter today and get insights like these delivered directly to your inbox each month.